Exchanges:

Public Exchanges

The Affordable Care Act (ACA) calls for the creation of state-based competitive marketplaces, known as Affordable Health Insurance Exchanges (Exchanges), for individuals and small businesses to purchase private health insurance. According to the Department of Health and Human Services (HHS), the Exchanges will allow for direct comparisons of private health insurance options on the basis of price, quality and other factors and will coordinate eligibility for premium tax credits and other affordability programs. ACA requires the Exchanges to become operational in 2014.

Due to a number of factors, states’ progress toward developing the Exchanges has been far from uniform. There has also been uncertainty surrounding the structure of the Exchanges and the role of entities that have been traditionally involved with the insurance placement process, such as brokers and agents.

On March 27, 2012, HHS issued final regulations to provide a framework for states on important aspects

of

Exchanges.

In addition to ACA’s Exchanges, private health insurance exchanges are emerging to provide another way for employers to provide health insurance coverage for employees.

State Progress on Exchanges

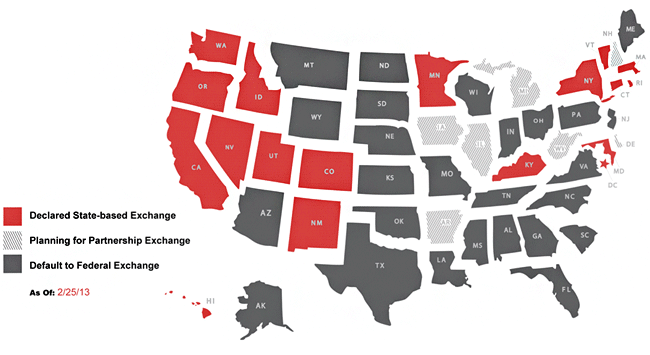

According to HHS, since ACA was passed in March 2010, all states have taken some action to implement the health care reform law. For example, 49 states are participating in ACA’s premium rate review system where insurers must justify the rationale behind any double-digit increases in insurance premiums. However, states have not made nearly as much progress toward establishing their Exchanges.

Exchanges must be ready to accept enrollees on Oct. 1, 2013. To meet this deadline, a state’s plan to operate its own Exchange must be approved by HHS no later than January 1, 2013. HHS will give conditional approval for a state’s plan if the state is advanced in its preparation but cannot demonstrate complete readiness by January 1, 2013. If a state fails to meet this deadline, HHS will operate the federally-run exchange for residents of that state.

HHS provided a Blueprint for states to use to receive federal approval for a state-based Exchange or a state-partnership Exchange. HHS also issued guidance on its approach to implementing a federally-run Exchange in any state where a state-based Exchange is not operating.

Some states, such as Oregon, Colorado and Maryland, plus the District of Columbia, have already established Exchanges and received HHS’ conditional approval for their Exchange plans. Other states that intend to operate their own Exchanges starting in 2014 include Kentucky, New York, Connecticut, Washington, Nevada, Idaho, Utah, New Mexico, Minnesota, California, Vermont and Rhode Island.

Some states have announced that they do not intend to create their own Exchanges, but will partner with HHS to develop an Exchange. These states include Iowa, Arkansas, Illinois, Michigan, West Virginia, Delaware and New Hampshire.

A majority of states will let HHS run an Exchange for their residents starting in 2014, including Arizona, Texas, Louisiana, Wisconsin, Florida, Georgia, Ohio and Pennsylvania.

Exchange Functions & Roles

The Exchanges will perform a variety of functions, including:

- Certifying health plans as qualified health plans (QHPs) to be offered in the Exchange;

- Operating a website to facilitate comparisons among QHPs for consumers;

- Operating a toll-free hotline for consumer support, providing grant funding to entities called “Navigators” for consumer assistance and conducting consumer outreach and education;

- Determining eligibility of consumers for enrollment in QHPs and for insurance affordability programs (such as premium tax credits, Medicaid and CHIP state-established basic health plans); and

- Facilitating the enrollment of consumers in QHPs.

States have flexibility in determining the design of their Exchanges. For example, states may decide whether their Exchanges will be operated by a non-profit organization or a public agency. States may also select the number and type of health plans available in their Exchanges and may determine some of the standards for QHPs, including the definition of required essential health benefits. In addition, states have flexibility to determine a role for agents and brokers, including the use of online brokers, in connection with

the Exchanges.

Additional Resources

HHS’s final regulations on Exchanges are available at: www.gpo.gov/fdsys/pkg/FR-2012-03-27/pdf/2012-6125.pdf.

More information on the Exchanges is available through www.healthcare.gov and http://cciio.cms.gov/index.html