Employer Penalties for Not Offering Coverage

(Delayed Until 2015)

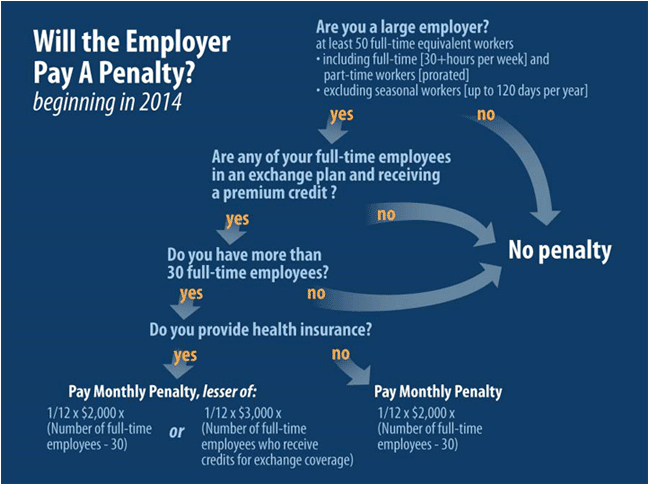

Employers with 50 or more employees (including full-time and full-time equivalent employees) that do not offer health coverage to their full-time employees (and dependents) that is affordable and provides minimum value will be subject to penalties if any full-time employee receives a government subsidy for health coverage through an Exchange. The sections of the health care reform law that contain the penalty requirements are known as the “shared responsibility” provisions.

The size of the employer for the shared responsibility rule is based on the average size for the prior calendar year. Part-time employees are included in the calculation according to a formula but are not required to be offered coverage. Special rules apply to counting seasonal employees, foreign employees and temporary agency employees. Companies with common ownership may have to be combined for purposes of this rule.

The penalty amount for not offering health coverage is up to $2,000 annually for each full-time employee, excluding the first 30 employees. Under proposed IRS regulations, an employer would not be liable for this penalty if it offers coverage to all but five percent (or, if greater, five) of its full-time employees and dependents.

Employers who offer health coverage, but whose employees receive tax credits because the coverage is unaffordable or does not provide minimum value, will be subject to a fine of up to $3,000 annually for each full-time employee receiving a tax credit, with a maximum annual fine of $2,000 per full-time employee (excluding the first 30 employees).

The IRS has provided safe harbor guidance for employers on determining who is considered a full-time employee (and must be offered coverage), along with how to measure a plan’s affordability and how penalties will apply when there is a waiting period for coverage. Guidance has also been issued on ways to determine a plan’s minimum value, including a calculator.

The proposed regulations also provide transition relief for non-calendar year plans, or fiscal year plans. The transition relief applies with respect to employees who would be eligible for employer-sponsored coverage as of the first day of the fiscal plan year starting in 2014 under the plan’s eligibility terms as in effect on Dec. 27, 2012. If these employees are offered affordable, minimum value coverage no later than the first day of the plan year starting in 2014, the employer will not be assessed a shared responsibility penalty with respect to these employees for any period in 2014 prior to the beginning of the plan year that starts in 2014 and runs into 2015.

Second, if an employer offered coverage under a fiscal year plan to at least one-third of its employees (full-time and part-time) at the most recent open enrollment period before Dec. 27, 2012 (or if the fiscal year plan covered at least one quarter of the employer’s employees), the employer will not be subject to a shared responsibility payment with respect to any of its full-time employees until the first day of the plan year starting in 2014, provided that those full-time employees are offered affordable coverage that provides minimum value no later than that first day. For purposes of determining whether the plan covers at least one quarter of the employer’s employees, an employer may look at any day between Oct. 31, 2012 and Dec. 27, 2012.

Reporting of coverage provided will be required for employers subject to the shared responsibility rules. Further guidance on the reporting requirement is anticipated. Employers will have to report information on the design and cost of their plans, applicable waiting periods and employees covered by the plan.

Determining If an Employer Will Pay a Penalty

Source: Congressional Research Service

Action Items – Determine Employer Size

- Count the number of employees according to the steps below to determine whether the employer will be subject to the share responsibility provisions. Include common law employees in the calculation and count employees of all related companies according to the IRS controlled group and affiliated service group rules in Code section 414. Rather than using the full 12 months of 2013 to measure whether it has 50 or more employees, the proposed IRS regulations allow employers to use any consecutive six-month period in 2013.

- Calculate the number of full-time employees (including seasonal employees) for each calendar month in the preceding calendar year. A full-time employee for any month is an employee who is employed on average for at least 30 hours of service per week.

- Calculate the number of full-time equivalent employees (including seasonal employees) for each calendar month in the preceding calendar year by calculating the aggregate number of hours of service (but not more than 120 hours of service for any employee) for all employees who were not full-time employees for that month and dividing the total hours of service by 120.

- Add the number of full-time employees and full-time equivalent employees (including fractions) calculated above for each of the 12 months in the preceding calendar year.

- Add up the 12 monthly numbers from the preceding step and divide the sum by 12. Disregard fractions.

Action Items – Determine Whether Coverage Is Offered to Full-time Employees (and Dependents)

- To predict whether an employer will be subject to a shared responsibility penalty, determine whether the employer offers coverage to substantially all full-time employees (and dependents).

- Coverage need not be provided during a permissible waiting period.

- All common law employees that work an average of 30 hours per week or more must be considered full time.

- If the employer has variable hour or seasonal employees where it is uncertain if they will work the requisite number of hours, establish a measurement period of 3-12 months to determine the average hours worked, in accordance with the separate rules for ongoing and new employees.

- If measurement periods are established for an employee, establish a stability period that is at least six months long and as long as the measurement period for treating the employee as full-time or not, depending on the results of the measurement period. An administrative period of up to 90 days may be established as well.

Action Items – Determine Whether Coverage Offered Is Affordable

- To predict whether an employer will be subject to a penalty for not providing affordable coverage, assess the affordability of the employer’s health coverage under one of the IRS’s affordability safe harbors.

- Under the Form W-2 safe harbor, determine if the employee portion of the self-only premium does not exceed 9.5 percent of the employee’s W-2 wages.

- Under the rate of pay safe harbor, determine if coverage is affordable based on an employee’s rate of pay. The employee's monthly contribution amount (for the self-only premium) is affordable if it is equal to or lower than 9.5 percent of the computed monthly wages.

- Under the federal poverty line safe harbor, affordability is determined based on the federal poverty line (FPL) for a single individual. Under this safe harbor, employer-provided coverage offered to an employee is considered affordable if the employee’s cost for self-only coverage does not exceed 9.5 percent of the FPL for a single individual.

Action Items – Determine Whether Coverage Offered Provides Minimum Value

- Review whether the plan provides minimum value by covering at least 60 percent of the cost of benefits. To make this determination, use one of the three available methods (minimum value calculator, safe harbor checklists or actuarial certification). Federal agencies have not yet released the safe harbor checklists.

- Under the calculator approach, enter plan design data into the minimum value calculator to determine minimum value.

- Once the safe harbor checklists are issued by federal agencies, they can be used to determine if the plan provides minimum value. If the plan’s terms are consistent with or more generous than any one of the safe harbor checklists, the plan will be treated as providing minimum value.

- If neither the calculator nor the checklists can be used because a plan has nonstandard features, seek an actuary’s certification that the plan provides minimum value.

Actions Items – Required Reporting

- In 2015, provide required information regarding plan coverage and participation in accordance with information return requirements.